Prospects for the euro based on the ECB policy

Omitting such risk factors as the US trade wars and the UK exit process from the EU, the monetary policy of the European Central Bank (ECB) remains extremely soft and one that acts as a major factor in the decline of the euro. Of course, it is worth noting the difficult global economic situation, not to mention the internal problems of the eurozone in France, and not to mention the indicators of the eurozone economy.

Despite all this, the ECB’s policy is a fundamental factor in the weakness of the euro. It is indicated by lower forecasts for economic growth and inflation in the eurozone. The main factor continues to be the reinvestment policy, which is a leading factor in the fact that the ECB will not raise rates.

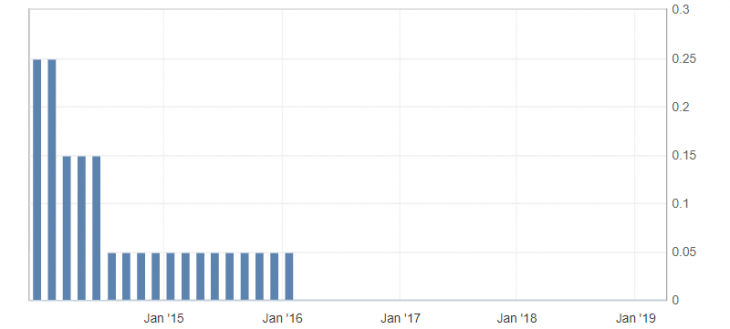

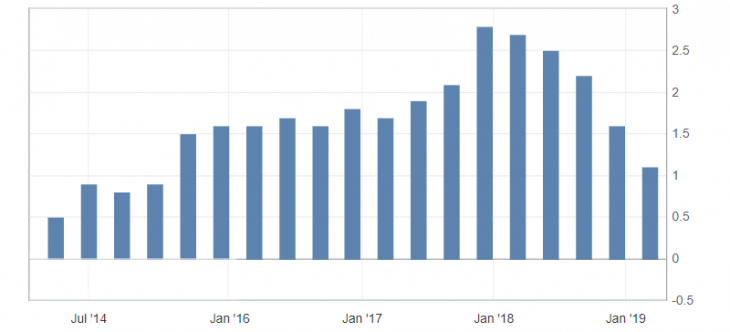

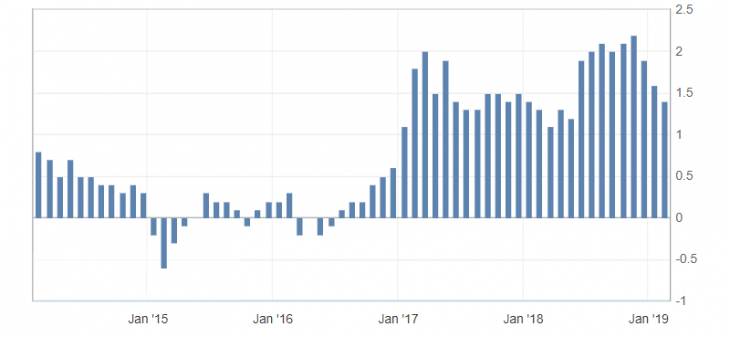

Let’s draw a parallel between the eurozone interest rates and GDP and inflation – the key parameters that the ECB relies on.

Fig. 1. ECB interest rate chart

Fig. 2. Eurozone GDP chart

Fig. 3. Eurozone consumer price index (CPI) chart

In this case, the increase in interest rates in the eurozone was supposed to fall on the beginning of 2017 and 2018. It did not happen because of the stimulus program. In the conditions of preservation of the existing downward dynamics of GDP and inflation in the Eurozone, which can be traced on the charts, one should have expected more reduction in rates from the ECB than their increase.

Adhering to zero rate policy the ECB will continue to put pressure on the single currency. So, the euro will remain under the pressure against the US dollar, as a more profitable currency, which can be traced in the market.

Technically, the EUR/USD currency pair remains in a downward trend in 2018. The key support of the euro against the US dollar is located near the lows of November 2018 (1.1210) and March 2019 (1.1180).

A break of this support zone will point to a new wave of euro sales against the US dollar and open the way to support levels of 1.1100 and 1.1070-50. This in fact does not act as a significant limitation for a longer perspective and while maintaining the soft policies of the ECB.

Summing up, it can be said that the ECB, in the conditions of preserving the existing government and the macroeconomic situation, is more likely to maintain or even reduce rates in the current year than to raise rates and tighten monetary policy.

Anton Hanzenko